Blog

Click here to go back

QuickBooks P&L. What is Gross Profit?

If you are like most people, every time you look at a profit and loss report in QuickBooks, you probably focus on two numbers. Total Income is one. How are sales or revenue going? Above expectations? About right? Or, the worst possibility, below expectations?

The second number you are likely to examine is the bottom line. Net Profit. Are we making or losing money. If making money, how much?

The profit and loss report can tell us much more. Most of you will have a line on this report labeled Gross Profit. What is that?

As with all financial reports, the accuracy of the profit and loss report depends not only the accuracy of the transactions entered into QuickBooks, but the setup of your chart of accounts as well.

The Gross Profit line is computed by taking the total income (or revenue) for the period and subtracting the balances in all Cost of Goods Sold type of accounts. So, what are Cost of Goods Sold type of accounts?

You have to look a little to find this account type in the window QuickBooks displays for creating new accounts, but it’s there.

In QuickBooks’ design, Cost of Goods Sold type of accounts are basically direct costs. If your business bought and sold inventory, the item setup for the inventory you sell will ask for a cost of goods sold account. The amount represents the cost of product you sold for a given time period.

But, we use this same account type in other kinds of businesses as well. What are the direct costs of producing the goods or services you sell?

A machine shop would create COGS type accounts for the materials purchased to fabricate the equipment being created on the shop floor. A contractor would use COGS type accounts for materials purchased for jobs, subcontractors, etc. Any cost that can be tied directly to a certain job or project.

How is this helpful?

The use of COGS type of accounts allows small business to divide their expenses into two major categories. Direct costs of production and indirect costs, or overhead. These two types of expenses act very differently as the business ebbs and flows, another topic for another day.

Most of us want to have some idea of what it costs to produce a service or product we sell to customers. How else would we decide what to charge the customer? The Cost of Goods Sold section of the profit and loss report tells us how close we are to meeting that target.

It’s usually a real advantage to view this as a percentage. As sales go up and down, the percentage of gross profit should change little.

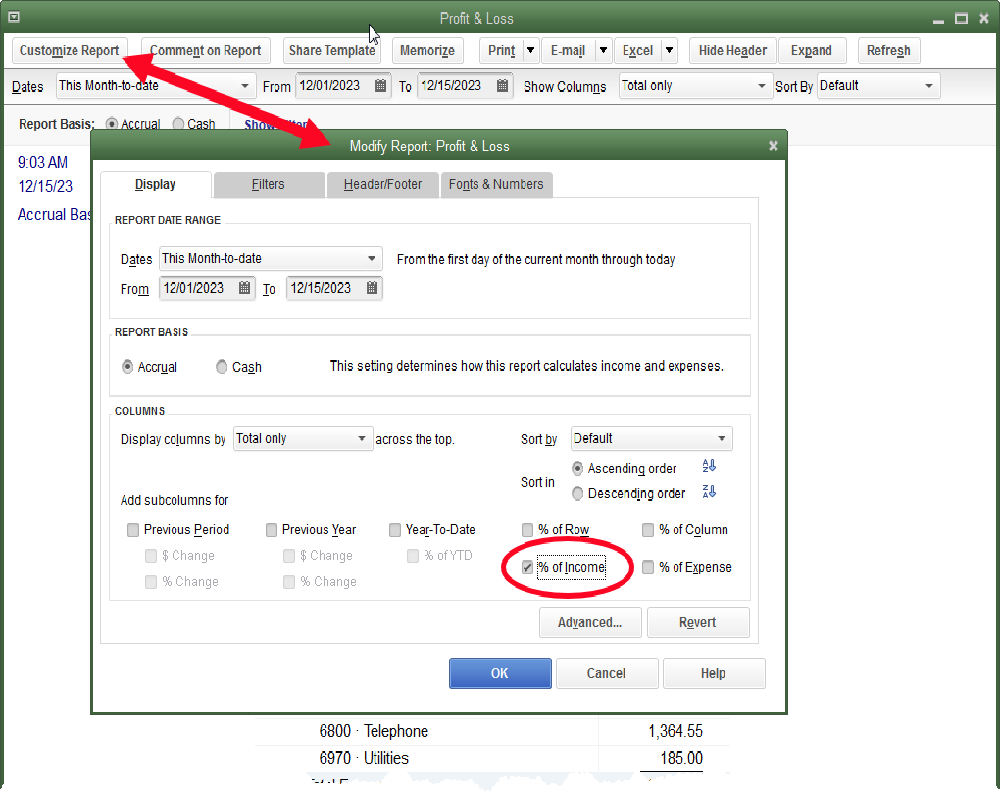

You can add a percentage column to your QuickBooks profit and loss report as shown below:

With the percent column added, this sample company’s profit and loss looks like this:

The gross profit (or margin) for Quality Construction so far in December is about 33%. The direct costs of the jobs they have completed then, is about 67%.

Considering Quality Construction eked out a minimal profit during this period, one consideration will be, is this a suitable margin for their business? What is the margin they aim for?

If they plan on a margin of 35% on the jobs they bid, they’ve underbid the jobs they completed in this time period. That, or some unusual event escalated costs beyond what they should have been.

If the margin is about right, then something in overhead, or indirect costs is too high for this level of sales. This possibility would require an examination of the QuickBooks Expense type of accounts and the amounts of those costs on the profit and loss report.